Executive summary

This quick report analyses the impact of the US-Iranian conflict on the dry bulk shipping sector, focusing on trade volumes, operational changes, and market forecasts for 2026.

The conflict involving the US, Israel, and Iran has significant consequences for the global maritime network. While tankers and LNG carriers are most directly affected, the dry bulk market is experiencing disruptions due to the closure of the Strait of Hormuz and increased security risks in the Red Sea.

1. Analysis of export and import trades

Dry bulk trade within the Arabian Gulf accounts for approximately 3% of global dry bulk trade.

Export trends

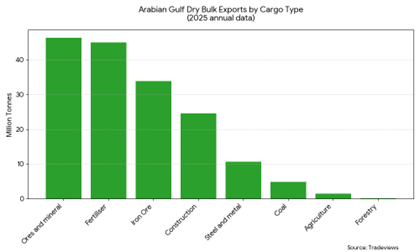

In 2025, exports from the region totalled approximately 160 million tonnes. The following figures are all for 2025:

- Destinations: India and Pakistan are the primary receivers, representing 44.7% of these exports, predominantly short-sea trades of limestone and gypsum.

- Commodities: The main export groups are ores and minerals (46.3 million tonnes), fertilisers (45 million tonnes), and iron ore (33.9 million tonnes).

- Fertiliser supply chain: The main fertilisers are sulphur (20 million tonnes), nitrogen (16.4 million tonnes), and compound fertilisers (6.9 million tonnes). Approximately 50% of global sulphur trade originates from the Arabian Gulf. Disruptions may force importers like China to substitute supplies via rail from Kazakhstan or seek long-haul alternatives from North America. We believe nitrogen is more widely available elsewhere; the Arabian Gulf represents 16% of global nitrogen trade.

Import trends

Imports to the region are approximately 130 million tonnes.

- Primary cargoes: Agriculture (50 million tonnes) and iron ore (32.6 million tonnes) are the leading imports. However, the iron ore pelletising plants mean the majority heads back out to Asia, so the net impact is negligible.

- Tonne-mile impact: A significant portion of these cargoes originates from the East Coast of South America (ECSA), resulting in high tonne-mile requirements — so any stoppage may dent Panamax trades.

2. Vessel distribution and operational shifts

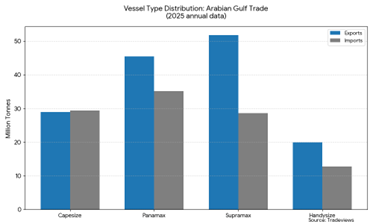

The regional trade relies on a variety of vessel sizes, with Supramax and Panamax vessels handling the largest share of exports.

- Export vessel usage: Supramax vessels lead with approximately 51.7 million tonnes, followed by Panamax (45.4 million tonnes), Capesize (29 million tonnes), and Handysize (20 million tonnes).

Operational impacts

The conflict has introduced two major operational variables:

- Rerouting: Threats in the Red Sea and the Suez Canal will lead more vessels to take the longer route around the Cape of Good Hope, significantly increasing transit times.

- Fuel costs and speed: Crude oil prices have increased by approximately $20 per barrel. To offset higher fuel costs, owners are increasingly adopting slow steaming, decreasing the efficiency of the fleet.

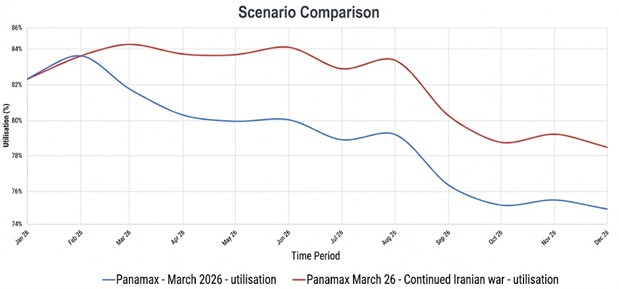

3. Impact on charter rates

Modelling suggests that the operational changes (rerouting and slow steaming) will have a more substantial impact on charter rates than the direct disruption of regional trade.

- Trade adjustment impact: Increased tonne-miles for replacing regional commodities (e.g. limestone from Spain or Canada instead of the Gulf) are estimated to increase charter rates by less than $500 per day. With some vessels trapped in the Arabian Gulf, the trade impact is largely a wash for most cargoes.

- Operational impact: Rerouting and slow steaming are expected to drive rate increases of between $2,000 and $3,000 per day.

- Largest effect will be on Panamax and Supramax vessels.

Source: Tradeviews.

4. Strategic geopolitical factors

The broader dry bulk market is currently supported by strategic stockpiling driven by geopolitical uncertainty, and these recent events will accelerate that need.

- China’s strategy: China has been importing volumes of iron ore and bauxite well above its consumption needs to build strategic reserves.

- US “Project Vault”: The US has responded with a $12 billion strategic mineral stockpile initiative.

- Outlook: These stocking policies are expected to keep dry cargo rates strong through 2026. However, the market faces a potential correction when these nations return to consumption-based import levels.