The supportive case — and why it’s not playing out

We’ve been analysing the impact of the recent bunker price spike on freight markets. At first glance, the effect should be supportive:

Higher bunkers → slower steaming → reduced effective fleet → higher rates.

But that’s not what we’re seeing.

What’s actually happening

Bunker prices have risen sharply, and the fleet is responding with:

- slower steaming

- longer voyage durations

This is tightening effective supply. However, the positive effect is currently being offset by behaviour on the demand side.

The key dynamic

Charterers appear reluctant to commit tonnage. The prevailing view in the market is that:

- the bunker spike is temporary

- freight costs may fall again in the near term

As a result, cargo is being delayed rather than moved.

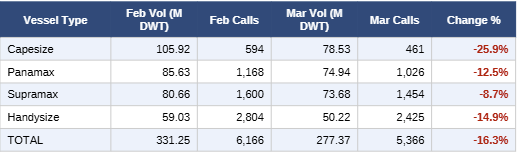

What the data shows

We compared the first two weeks of February against the first two weeks of March, using port call activity to derive DWT demand.

The result:

- Capesize demand down ~25%

- Supramax demand down ~8.7%

Higher voyage costs are discouraging long-haul cargoes. This confirms that demand is softening faster than fleet inefficiency is tightening. There are also reduced cargoes moving to the Middle East.

What happens next

If bunker prices fall, we would expect a release of delayed cargo demand. This could lead to:

- a short-term surge in volumes

- tightening utilisation

- upward pressure on freight rates

Takeaway

For now, the behavioural response to bunker prices slightly outweighs the effective supply reduction — but this may reverse quickly if sentiment shifts.

We’re currently modelling how supply and demand changes could translate into freight rate scenarios over the coming months.