The Panamax market firmed materially through the spring on a coal-led move — coal being the sector’s usual swing factor, weak through last year and turned sharply by the Middle East energy shock, while iron ore stayed firm in the background. The leading leg, Southeast Asia, is now cresting. The more important point, though, is forward: a cluster of supply-side forces is lining up that could carry the firm market through to a strong finish to the year. This note recaps how we got here, then sets out that forward case.

How we got here

Iron ore has been the steady backbone of Panamax demand and held up well. Coal is the sector’s usual swing factor, and after a weak last year it is what turned this spring. With Gulf LNG disrupted by the closure of the Strait of Hormuz, power generators switched back to coal, and the clearest, cleanest signal is Southeast Asia: its seaborne coal tonne-miles reached a multi-year high in April and, on our forecast, the highest monthly reading in three years in May — around a fifth above the prior two-year average for the quarter. Atlantic coal out of Russia and South Africa stayed elevated too. Coal is carried chiefly on Panamax and Capesize tonnage, so the move lifted voyage-day demand across the larger sizes from March onward. Northeast Asia firmed too, although by less than its headline year-on-year suggests, which flatters an unusually weak April 2025; the weight of the move sits with Southeast Asia and the Atlantic.

A note on measures: we model demand primarily in tonne-days, which give the fuller picture of vessel employment. We lean on tonne-miles here because they make the point plainly — more coal is moving, and it is travelling from further afield.

The regional picture

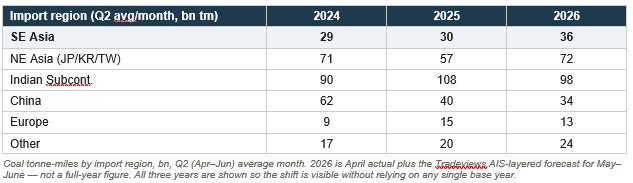

Aggregate coal tonne-miles are little changed on two years ago — the story is the reshuffle underneath, which the three-year columns make plain. Southeast Asia is the clear, sustained gainer, climbing each year (29 → 30 → 36) as Indonesian supply restraint draws buyers onto more distant tonnage. China has fallen structurally, from around 62 to 34, and is now the market’s main swing and downside risk. The Indian Subcontinent remains the single largest block; it peaked in 2025 and has eased since, making it the obvious candidate to rebuild. Northeast Asia is best read as a round-trip — 71 to 57 and back to 72 — a recovery from a weak 2025 rather than fresh growth. The strength is in where coal goes and how far it travels, not in the headline volume.

The forward case

Several supply-side forces point the same way into the second half. Individually each is incremental; together they make a firm — potentially strong — finish to the year the base case rather than the upside.

• Indonesia’s supply restraint: Indonesia set out this year to rein in coal supply and support prices, and that appears to have happened. The effect has been to draw down Southeast Asian stocks, leaving the region importing more — and from further afield — to cover the gap. That is the tonne-mile effect in action: more coal moving, over longer distances.

• Restocking and supply-chain security: with inventories run down and supply-chain security now front of mind for most importers, the likely response over the coming months is to rebuild stocks — forward demand that has yet to be placed.

• A Hormuz cargo backlog: the disruption around the Strait of Hormuz has left a backlog of cargoes still to work through, which should support voyage demand as flows normalise.

• Weather risk to supply: an El Niño pattern threatens mining and loading in Australia and South America, a further potential tightener on the supply side into year-end.

The balance of risk

The clearest two-way risk is China. A safety incident at a Chinese coal mine has prompted reviews across others that could curb domestic output and pull in more seaborne coal; but Chinese buyers are highly price-sensitive, and with comfortable stockpiles the import response may stay muted. The other swing is the Strait of Hormuz: a durable normalisation that lets Gulf LNG return would ease the gas-to-coal premium. On balance, with Southeast Asia restocking, supply restraint biting and weather risk rising, the forward setup leans firm into the close of the year.