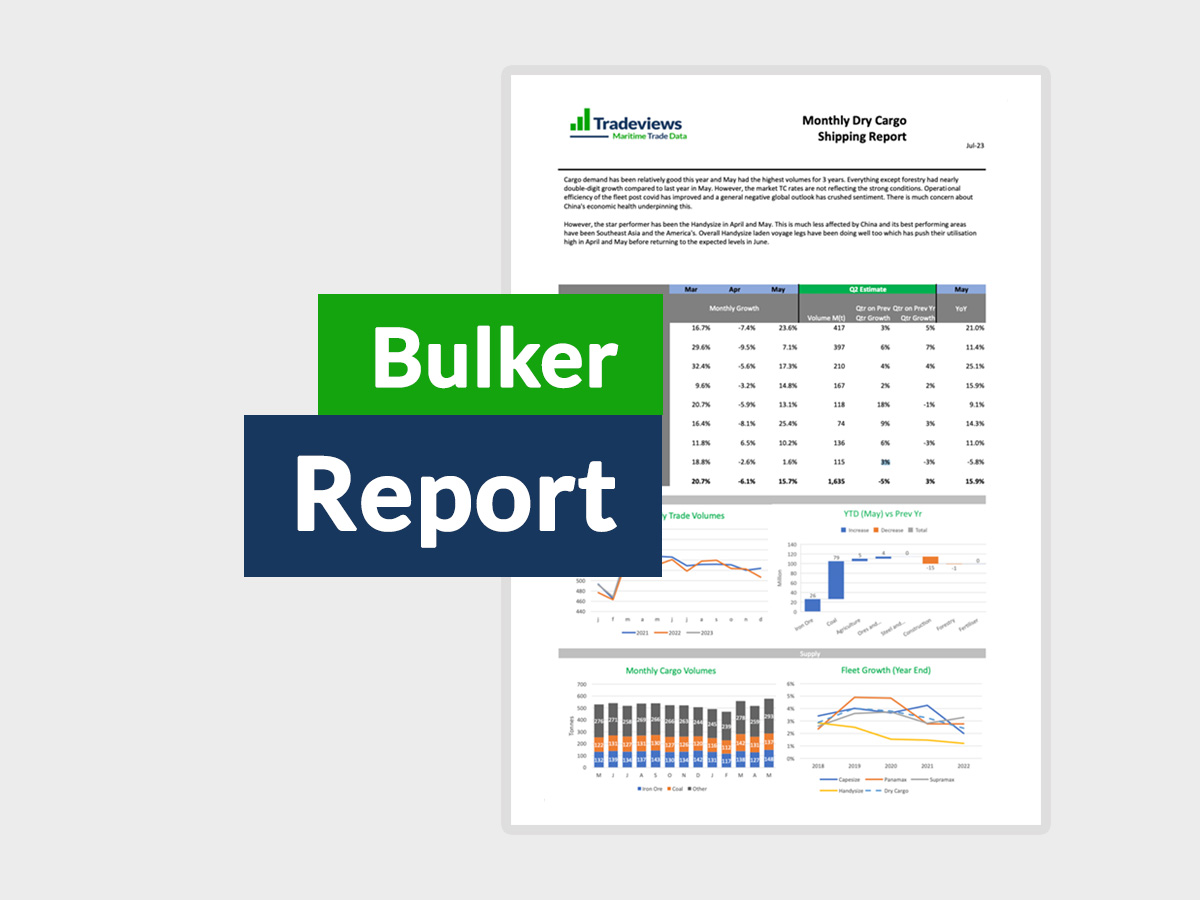

Cargo demand has been relatively good this year and May had the highest volumes for 3 years. Everything except forestry had nearly double-digit growth compared to last year in May. However, the market TC rates are not reflecting the strong conditions. Operational efficiency of the fleet post covid has improved and a general negative global outlook has crushed sentiment. There is much concern about China’s economic health underpinning this.

However, the star performer has been the Handysize in April and May. This is much less affected by China and its best performing areas have been Southeast Asia and the America’s. Overall Handysize laden voyage legs have been doing well too which has push their utilisation high in April and May before returning to the expected levels in June.